In the challenging macroeconomic environment, distractions are everywhere. While we are aware of the prevailing market conditions, our focus remains on identifying and investing in a select universe of companies that meet our four investment pillars:

- A quality business (as defined by solid organic growth and healthy/growing ROIC);

- A strong balance sheet;

- Owner-minded management with strong capital allocation; and

- A fair (or better than fair) acquisition price.

We believe consistently predicting what events will occur during our investment time frame, and the market’s reaction to these events, is highly unlikely. Instead, we rely on our portfolio of high-quality businesses continuing to execute through both the good and the bad times. An ability to deliver sustainable earnings growth is what we believe drives share price appreciation over the long term. Confidence in the strength and resilience of the underlying businesses, across cycles, is thus critical to our confidence in our portfolio positions.

Below, we will touch on a portfolio example of why we believe it pays to think long-term, and how we attempt to avoid reacting to market noise, so as to not get in the way of compounding.

Aon (NYSE: AON)

A portfolio stalwart since its inclusion in October 2018 and a global leader in risk, retirement, and health solutions, the company has been rock-solid in its operational execution. Over the last decade, Aon has averaged 4% organic revenue growth, while management has delivered very solid cost control. This resulted in the adjusted operating margins increasing approximately 1,300 basis points, and ~12% adjusted earnings per share (EPS) growth p.a. over the period. With high margins and limited capital needs, the company has generated large amounts of free cash flow, averaging close to 120% free cash conversion over the same timeframe.

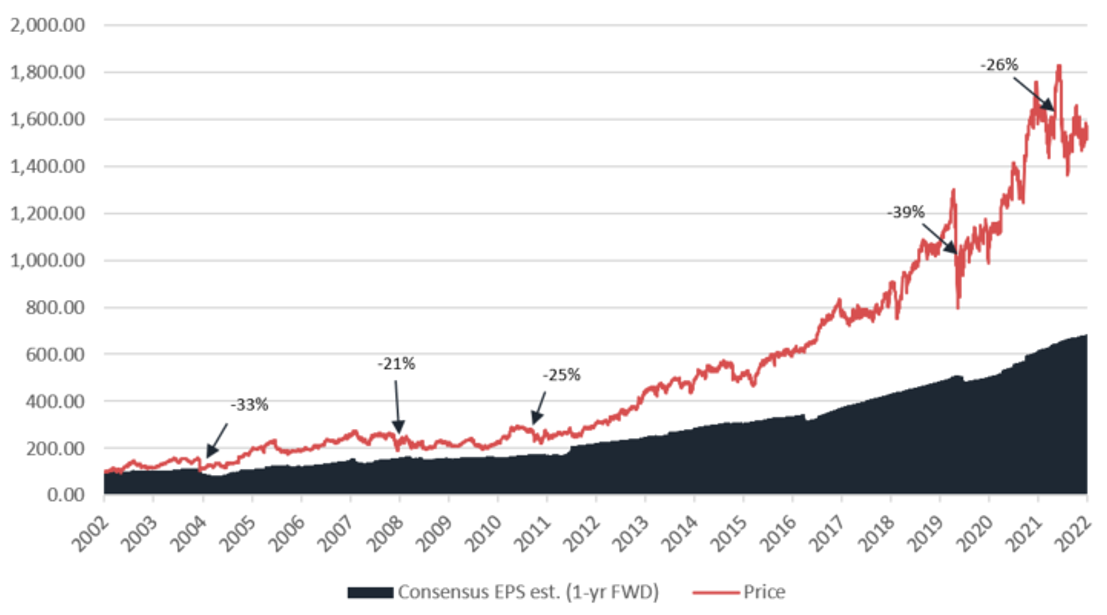

Over a 20-year period (encompassing the Financial Crisis), the market’s recognition of Aon’s compounding power becomes apparent.

For the 20 years to current(1) , we evaluate the cumulative average growth rate (or CAGRs) for both earnings and price:

- Diluted EPS (Non-GAAP): 11.0%(2)

- Share price: 14.7%

- Total shareholder return: 1,544% (over 15x your initial investment)

For context, the S&P500 grew at a 7.7% CAGR over the same period (a total return of 439%).

During this period, however, we saw significant stock price swings (both up and down), with far greater share price volatility than earnings volatility.

The chart below highlights this graphically, plotting Aon’s share price (the red line) against the consensus earnings expectations for the company (the blue line)(3) . While both price and earnings have trended upwards over time, there are numerous instances when Aon’s stock price fell over 20%, due to both macroeconomic and company-specific concerns.

This chart demonstrates the consistency of Aon’s earnings growth and the power of compounding - both for Aon’s earnings and the share price over the long term. As we would expect, the share price has broadly tracked earnings over this long-time horizon. The chart also highlights the potential rewards of finding and investing in quality companies, and then getting out of the way and letting compounding do its thing. Consider the money left on the table if you sold out of Aon in the early 2000’s, on one of the instances when the headlines flashed danger and you dashed to “safety”.

Chart 1: Aon’s rolling consensus NTM earnings estimates vs. price, indexed over the last 20 years (to current)

Source: FactSet. Past performance is not a reliable indicator of future performance

A key to Aon’s compounding over the last two decades is earnings consistency. So how does Aon so consistently deliver?

- End market dynamics and positioning – industry concentration is high, and Aon and Marsh McLennan dominate the top end of the market with high barriers to entry. In such a market, you must have a truly global presence, the ability to hire the best talent and solve the most complex insurance/risk management problems for clients. Further, given insurance needs are ongoing, as is advice around human resources and investment, the company boasts strong recurring revenues and retention rates of ~90% for its core insurance business. Such industry characteristics lead to consistent organic revenue growth over time.

- Solid expense control – over the last decade, the company has been able to significantly leverage their top line, boosting revenue productivity, and driving substantial operating margin improvement.

Aon’s stable top line and an ability to drive leverage over their cost base deliver an earnings stream that grows steadily and is relatively predictable, characteristics we value highly.

We see ourselves as long-term owners of a business, not short-term stock traders, and so seek businesses that perform across all environments. We strive to cut through the noise and attempt to refrain from overreacting to each new piece of news or economic data point that gets thrown at us each time we glance at our screens.

Taking on new information is important, however, sizing that new information and data against a trove of past evidence is essential.

In the case of Aon above, we can see compounding at work and the potential rewards from buying and holding a high-quality business with solid, sustainable earnings growth through time.

While we do not necessarily enjoy downward swings in our companies share prices (unless we are buying more!), we believe our all-weather businesses are apt to navigate their way through challenging periods. Given the businesses we look to own are typically market leaders with scale, unmatched competitive position, pricing power, fortress balance sheets, and have well-tenured management teams, we have confidence that they will be able to continue to compound earnings over the long term.

We don’t try and time the market

There’s a higher probability of us identifying great companies, that will prosper across many cycles, than us consistently forecasting macroeconomic conditions, or market highs and lows. As shown for Aon, selling out of a quality holding may disrupt incredible compounding and result in a large opportunity cost. Where we believe we have an appreciation of, and confidence in, a company’s durability and consistency, we do not attempt to time the market and put that potential compounding at risk.

So, we concentrate our efforts on identifying, researching, buying and holding high-quality businesses. This inevitably leads us to companies with commanding competitive positions that deliver sustainable organic growth and improving margins through the cycle. We believe that this will position our portfolio of companies to deliver healthy earnings growth over the long term.

High conviction investing

Claremont Global is a high-conviction portfolio of value-creating businesses at reasonable prices. Stay up to date with all our latest insights but clicking follow, or visit our fund profile below for more information.

Sources

(1) 16 November, 2022

(2) 2022 earnings uses the consensus estimate for non-GAAP EPS for FY22, for context, an average of the last five years’ 20-year diluted non-GAAP EPS CAGRs is 10.4%

(3) Earnings are displayed as the rolling one-year forward, consensus expectation

Disclaimer

The information in this article may contain general advice. Any general advice provided has been prepared without taking into account your objectives, financial situation or needs. Before acting on the advice, you should consider the appropriateness of the advice with regard to your objectives, financial situation and needs.

This information has been prepared by Claremont Funds Management Pty Ltd (Investment Manager) (ACN 649 280 142, ABN 38 649 280 142, CAR No. 001289207), as investment manager for the Claremont Global Fund (ARSN 166 708 792) and Claremont Global Fund (Hedged) (ARSN 166 708 407), which are together referred to as the ‘Funds’. Equity Trustees Limited (ACN 004 031 298, AFSL 240957) (“Equity Trustees”) is the Responsible Entity of the Funds. For further information on the Funds please refer to each Fund’s PDS which is available at www.claremontglobal.com.au. The Target Market Determination for the product can be available by contacting your adviser. A Target Market Determination is a document which is required to be made available from 5 October 2021. It describes who this financial product is likely to be appropriate for (i.e. the target market), and any conditions around how the product can be distributed to investors. It also describes the events or circumstances where the Target Market Determination for this financial product may need to be reviewed.

Past performance is not a reliable indicator of future performance.

This article may contain statements, opinions, projections, forecasts and other material (forward-looking statements), based on various assumptions. Those assumptions may or may not prove to be correct. The Investment Manager and its advisers (including all of their respective directors, consultants and/or employees, related bodies corporate and the directors, shareholders, managers, employees or agents of them) (Parties) do not make any representation as to the accuracy or likelihood of fulfilment of the forward-looking statements or any of the assumptions upon which they are based. Readers are cautioned not to place undue reliance on forward-looking statements and the Parties assume no obligation to update that information. The Parties give no warranty, representation or guarantee as to the accuracy, completeness or reliability of the information contained in this report. The Parties do not accept, except to the extent permitted by law, responsibility for any loss, claim, damages, costs or expenses arising out of, or in connection with, the information contained in this article. The information provided in the article is current at the time of publication. The views expressed herein should be considered as part of a wider portfolio investment strategy applicable to the Funds and should not be considered in isolation or relied on to make an investment decision without seeking further information and/or advice from a financial adviser.